The bubble faded, and only performance remained KOSPI ▲4,105.93 │ KOSDAQ ▲929.14│ KRW/USD▲1,480.14 |

|

|

As of 3:30 p.m. on the previous trading day |

|

|

✴ Keystone Partners╎In 2025, Keystone Partners focused on managing existing portfolios and clarifying exit prospects rather than expanding new investments, continuing results through the sale of Orion Technology and the push for Sena Technology’s IPO. Based on a track record of rapid investment execution and exits, the firm has been steadily raising blind funds, with evaluations saying it has reaffirmed its credibility and position as a mid-sized private equity firm.

✴ Bokwang Investment╎Bokwang Investment became embroiled in controversy over alleged violations of the Venture Investment Act after suspicions emerged that a former executive received advisory fees worth several hundred million Korean won in return for investments through a side agreement. If confirmed, concerns are growing that potential sanctions and damage to limited partner trust could weigh on future fund formation.

✴ Innovation Venture Organizations Council╎The Innovation Venture Organizations Council issued a joint statement welcoming the government’s 2025 announcement of its “Comprehensive Measures to Become One of the World’s Top Four Venture Powers,” lending support to the policy direction. Expectations in the venture ecosystem are rising as the measures reflect support for big tech growth tracks, expanded investment funding, and improvements to M&A and secondary markets, strengthening the virtuous cycle of growth and exits.

✴ IMM Holdings╎In 2025, amid an unfavorable buyout environment, IMM Private Equity took a cautious stance on new investments and adopted an exit-focused strategy. Instead, ICS, which oversees the group’s credit strategy, delivered strong returns through large-scale fundraising and rapid investment and recovery, with evaluations saying it drove overall group performance.

✴ Algnomics╎A technology transfer agreement with Eli Lilly supported corporate valuation during the listing process by demonstrating validation from a global pharmaceutical company. Combined with a conservative IPO valuation of about $206 million and entry into Phase 1 clinical trials, financial investors are assessed to be raising expectations for tenfold or higher returns.

✴ Q Capital Partners╎In 2025, Q Capital Partners prioritized operational normalization and stake expansion at Norang Tongdak and Chorokbaem Media rather than new investments. As Chorokbaem Media returned to profitability and Norang Tongdak showed improving earnings, the firm entered a phase of preparing mid- to long-term exit strategies based on value enhancement.

✴ POSCO Investment╎In 2025, POSCO Investment appointed Kim Geun-hwan as its new chief executive, undergoing another leadership change amid frequent CEO turnover. With four CEOs over two years since its conversion to a holdings CVC structure, attention is focused on whether the appointment can restore organizational stability and consistency in investment strategy.

✴ Praxis Capital╎Praxis Capital raised a blind fund of about $549 million and spun off a credit investment entity, completing preparations to move toward a larger-scale manager. While keeping investment execution cautious, it produced exit results from ENCOS and D&D Pharmatech, building both capital and track record at the same time.

✴ A-Stone Ventures╎Backed by commitments from public LP programs, A-Stone Ventures began forming an AI fund sized at about $17.1 million to $20.6 million, targeting formation in 2026. If completed, AUM will exceed about $68.6 million, stepping up as a mid-sized VC focused on AI convergence.

✴ Highland Equity Partners╎Alongside blind fund formation, Highland Equity Partners pursued bolt-on strategies and exit design in parallel through investments in Salady and Orion Technology. The firm expanded its platform with an operations-improvement strategy despite concentration toward large managers, but some investments also revealed the limitations of mid-sized PE through adjusted exit timelines.

✴ Taekwang Industrial╎Despite a downturn, Taekwang Industrial selected employees and teams that delivered cost reductions and improvements in facilities and processes and presented its 2025 internal awards, with evaluations saying it moved to strengthen its internal performance culture by officially recognizing on-site results.

✴ Kiwoom Investment╎Kiwoom Investment recovered about $44.6 million by selling part of its stake immediately after Quad Medicine’s listing, and total proceeds are expected to reach around $137.2 million including the remaining shares. Four years after the initial investment, the firm has entered the exit phase, with a fast exit showing an internal rate of return in the mid-to-high 20 percent range becoming visible.

|

|

|

Investment Industry Veteran Do Yong-hwan to Retire Before 2025 AGM |

|

|

⭑ Retirement timing follows a planned path

Do Yong-hwan, chairman of STIC Investment and a leading figure in Korea’s PEF and VC industry, recently stated in a keynote speech at a VC event that he plans to step down next year. Born in 1957, he will turn 70 in Korean age next year, and his term as an inside director runs through March 28, 2026, making an exit before the shareholders’ meeting a natural timing. Given that he has repeatedly mentioned retirement at age 70, the decision is widely seen as planned rather than sudden.

⭑ Full exit, not just management retirement?

His options may go beyond stepping down from executive roles. Market talk suggests he is also reviewing scenarios in which he sells his entire equity stake to a third party and leaves the company completely. He has reportedly contacted multiple potential buyers, and some companies interested in domestic PEF operations are said to have shown acquisition intent.

If realized, this would go beyond a personal retirement and become an event that reshapes STIC’s governance from the ground up. Unlike a partial retirement where the founder retains shares, a full sale would cut off even informal influence. It could also mark a turning point, shifting STIC from a founder-led firm to a financial company with separated ownership and management.

At the same time, such a move would raise the bar for market evaluation. Without the founder’s name or track record to lean on, future performance and decision-making would face much stricter scrutiny. In that sense, a stake sale is seen as the cleanest exit for the founder, but also the most difficult challenge left for the company.

⭑ Numbers that define a first-generation pioneer

Do founded STIC Investment in 1996, at a time when private equity itself was unfamiliar in Korea, and helped build the market’s basic framework from scratch. Rather than simply managing capital, he focused on designing fund structures and governance that institutional investors could trust.

His track record is symbolic. In 2018, STIC invested about $68.6 million in HYBE and later recovered roughly $651.6 million, a rare ten-bagger deal in Korea’s PEF and VC industry. The successful buyout of Daekyung O&T is also seen as proof that a growth-oriented manager can deliver results in control acquisitions.

On the back of these results, STIC’s cumulative assets under management have grown to about $6.4 billion, with more than 110 portfolio companies. The fact that major institutions such as the National Pension Service and the Korea Teachers' Pension entrust long-term capital to STIC underscores that it is no longer just a star player, but a fully institutionalized investment firm.

|

|

|

This retirement may appear, on the surface, to be a long-anticipated step, but when viewed together with its timing and environment, it also reflects a broader shift in industry sentiment. As activist funds have gained influence, market scrutiny of founder-centered governance structures has become far more demanding than in the past.

The issue of generational transition naturally follows. Looking at the current board structure at STIC Investment, there are figures positioned to manage an interim phase, but it is still early to say the firm has fully transitioned to a next-generation system. Once the founder’s track record and symbolic presence fade, the market will inevitably assess more directly how reliably the organization and its systems operate, rather than any individual.

The possibility of a full stake sale can be read in the same context. Unlike stepping back while retaining ownership, a complete divestment minimizes residual influence. At the same time, some interpret it as a signal of intent to transform STIC from a personal, founder-led firm into an institutionalized financial company. As a result, subsequent performance and decision-making are likely to be judged by much stricter standards.

Ultimately, this retirement can be seen as more than the conclusion of one individual’s career. It may mark a transition in which Korea’s first-generation private equity model moves to its next stage. The market’s focus is clear: whether large-scale investments can continue without the founder’s name, whether decision-making structures can sustain trust, and whether long-term strategy can remain intact under external pressure.

For that reason, this news does not end as a simple retirement story. Whether STIC after Do Yong-hwan is evaluated as a stable, system-driven organization, or placed on a sharper test that highlights the founder’s absence, will depend on the choices made and how they are executed from here. |

|

|

The bubble faded, and only performance remained |

|

|

⭑ So, are they making money now?

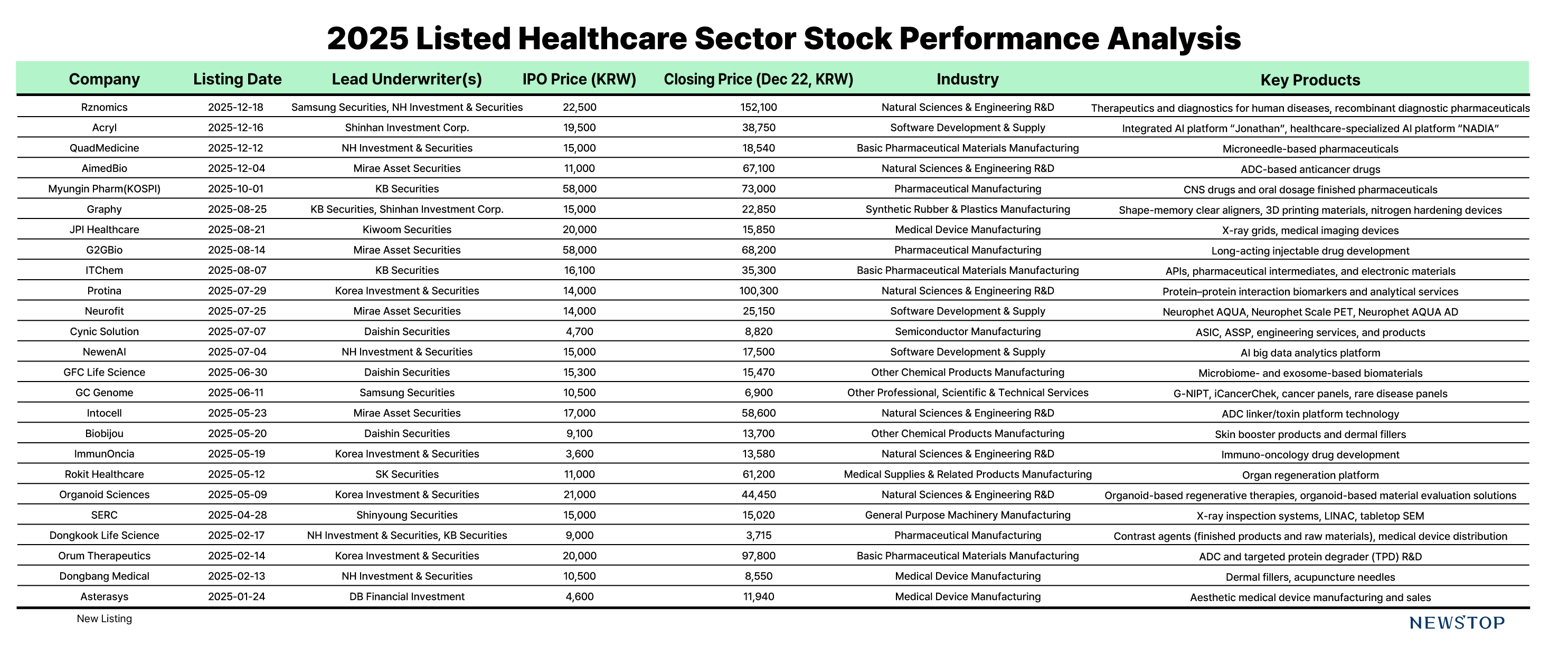

In the 2025 domestic IPO market, biotech and medical device companies are back at the center. But the atmosphere is completely different from before. A few years ago, companies could attract investors with nothing more than the potential of clinical pipelines or future growth stories. Large sums flowed in on expectations alone. As cases of weak performance after technology-based listings accumulated, however, the market learned its lesson. Now, only companies with already proven revenue structures, such as actual sales or global technology licensing, are being selected.

According to IB relatives the biotech market is now sharply divided by the presence or absence of earnings. The market’s question has shifted from Will it do well someday? to How much has it shown so far?

⭑ Money moved only to companies with results

This shift was immediately reflected in stock prices. DAC platform company Orum Therapeutics, despite having experienced a past clinical halt, saw its shares rise about fivefold, from $13.7 to $67.1, as its follow-up pipeline and platform competitiveness were recognized. It was valued not on clinical expectations, but on technology validation and business continuity.

There were even more dramatic cases. Algenomics, which achieved global technology licensing worth about $1.17 billion, surged from an IPO price of $15.4 to $104.3 in a short period. Protina rose about seven times its IPO price, and AimedBio jumped more than sixfold, clearly showing investors’ appetite for biotech companies with earnings.

Conversely, companies with only expectations and no results have been thoroughly ignored. Whether a firm has generated real income by earning recognition from global big pharma has become the decisive standard for valuation.

⭑ Fundamentals shown by the numbers

Improved performance is also visible in industry-wide data. Cumulative revenue of listed domestic biohealthcare companies in the first three quarters of 2025 rose by more than 11 percent year on year, with exports recording double-digit growth.

The Korea Bio Association attributes this to exports as the main driver. As products and technologies gain recognition in global markets, actual cash inflows have begun. Large companies expanded overseas CDMO orders, while smaller biotechs started to build meaningful revenue through technology licensing and commercialization pipelines.

Financial stability has also improved. Many listed companies maintained equity ratios above 70 percent, strengthening their balance sheets, which has become a key factor supporting IPO investor sentiment. As a result, the IPO market has clearly shifted toward asking about verified revenue structures before growth potential.

⭑ Will this trend continue?

Looking at year-end and early next year, the same pattern holds. Medical device company LBS Med, listing on the 24th, fixed its IPO price at the top of the band at $37.7, entering the market with a market capitalization of about $933 million. Mezzue, preparing for a 2026 listing in mobile remote patient monitoring, and Canaph Therapeutics, focused on human genome-based drug development, are also highlighting concrete business results and global licensing achievements.

If you were wondering, “Can biotech IPOs succeed again?” the answer is becoming clear, with one condition. Only companies that can show numbers are welcomed.

For investors, the criteria have actually become clearer. Instead of asking how many pipelines a biotech company has, it now makes sense to ask how large its licensing deals are and how much revenue it generated last year. The market has made its priorities clear.

How far this earnings-focused market will extend will again be answered by future numbers. But one thing is certain. The era of hype is over, and only biotech companies that truly make money will survive.

|

|

|

🛠 Fixing the Next Gap╎After Gmarket, E-Mart24

E-Mart is moving to restore competitiveness at its convenience store unit E-Mart24 after finding a turnaround path for Gmarket. The company is developing a next-generation franchise model that restructures customer traffic and product layout, aiming to increase both dwell time and purchase conversion. Based on this approach, it plans to add about 650 stores next year, seeking to offset scale disadvantages by improving franchisee profitability and offering differentiated customer experiences. |

|

|

🪙Locked in Crypto╎K Bank’s IPO Still Dependent on Upbit

K Bank has launched its third IPO attempt, but a large portion of its profit structure remains tied to deposits from Upbit. Deposit volumes fluctuate with volatility in the crypto market, while funding costs have risen sharply due to higher fee rates. Although the bank is expanding loans to individual business owners as a new growth pillar amid household lending regulations, assessments say it still lacks a clear equity story needed to persuade investors.

|

|

|

💳 Korea’s First IMA╎Korea Investment & Securities’ Initial Step

Korea Investment & Securities has launched the country’s first Integrated Management Account product as the inaugural licensed operator and opened subscriptions through the 23rd. The product invests client deposits in corporate loans, corporate bonds, and acquisition financing, distributing operating returns while carrying a principal repayment obligation. It is viewed as a regulated investment product linking wealth management and corporate finance, and as the starting point of the firm’s equity story aimed at expanding the domestic risk capital market. |

|

|

📈Self-funded Investment╎Qurient

Qurient invested about $6.9 million into its German subsidiary QLi5 Therapeutics, raising its ownership stake to 64 percent. The capital increase aims to accelerate development of PI payload technology, a next-generation ADC platform, with participation from Nobel laureate Robert Huber. As the potential for a broadly applicable payload that addresses existing ADC resistance has been identified, Qurient’s technology value is entering a critical validation phase in the global ADC market.

|

|

|

📊Year-end IPO Momentum╎KOSDAQ

Listings by Samjin Foods on December 22, LIVESMED on December 24, and SemiFive on December 29 are sustaining year-end IPO momentum. SemiFive attracted subscription deposits of about $10.75 billion, with expectations for AI chip demand, supported by its role as a design solution partner to Samsung Electronics, boosting investor sentiment. At the same time, Kanaph Therapeutics and Mezzoo have passed preliminary reviews, while Musinsa and K Bank are preparing filings, signaling an expanding IPO pipeline for next year. However, institutional demand may weaken due to December book closing, raising listing-day volatility, and valuation and overhang risks require close review. |

|

|

🥛Dairy Market Pressure╎Zero Tariffs Ahead

From 2026, tariffs on dairy products from the EU and the United States will fall to zero, likely accelerating imports of price-competitive sterilized milk. Import volumes have already increased more than fourfold over the past five years, with cafes and bakeries increasingly replacing domestically produced milk. In response, domestic producers such as Maeil Dairies, Seoul Milk, and Namyang Dairy are diversifying profit structures by strengthening premium product lines, expanding protein and plant-based beverages, and increasing B2B exposure. |

|

|

Every one of them is rich on social media. |

|

|

As the year-end approaches, the SNS landscape becomes increasingly skewed.

Due to platform dynamics, content related to travel, consumption, and performance signaling is more frequently exposed at year-end, and algorithms repeatedly amplify scenes that receive strong engagement. As a result, lifestyles that appear wealthier than the actual average are overrepresented. Year-end SNS is less a reflection of reality than a compressed display of top-tier consumption.

Certain scenes recur within this structure: overseas travel every season, high-end dining on anniversaries, and luxury product unboxing. It is difficult to view this purely as individual exhibitionism. It is more accurately the visible outcome of a social structure in which assets and consumption are concentrated at the top and reproduced on screen. With repeated exposure, one thought naturally arises.

“Is everyone doing well except me?”

A country with a large wealthy population, by the numbers

According to a 2025 wealth report, individuals holding at least $686,000 in financial assets number about 476,000, or roughly 0.92 percent of the population. Despite their small share, this group controls 60.8 percent of total household financial assets.

It is important to note that these figures cover only financial assets such as deposits, equities, funds, and insurance. Real estate is excluded. This helps explain why perceived inequality often feels stronger than what headline numbers suggest.

The wealthy, and the wealthiest among them

Even within the wealthy group, asset concentration is moving rapidly upward. Ultra-high-net-worth individuals, defined as those holding more than $20.6 million, account for 46 percent of the group’s total $2.1 trillion in financial assets, equivalent to about $968 billion.

By contrast, those holding between $686,000 and $6.86 million (₩1 billion to ₩10 billion) account for a smaller and declining share. Growth rates also diverge. While the total number of asset holders increased only modestly over the past year, the ultra-high-net-worth population expanded at a much faster pace. The data shows a structure in which larger asset bases grow more quickly.

Not born early enough

This is where perceived deprivation becomes most tangible. Households headed by someone under 39 hold an average net worth of about $151,000, down 0.9 percent from the previous year. This was the only age group to record an asset decline.

Among the wealthy, asset allocation is also shifting. Real estate accounts for a smaller share than before, while interest in alternative assets such as precious metals and digital assets is rising. The direction is clear. Rather than catching up through labor income, opportunities increasingly expand through assets already owned. In such an environment, younger generations starting from a weaker position are structurally disadvantaged.

If the world seen on social media has felt especially distant, this structure may be the reason. In an era where wealth compounds upward, this experience is not unique.

|

|

|

✴ Equity Story

An Equity Story is a company’s investment logic used to explain itself to the capital market.

Simply put, it is a story that explains, from an investor’s perspective, why the company’s stock is valuable. It is not a simple performance explanation or promotional message, but a narrative structure that connects the company’s current value with future expectations.

The first question investors always ask is the same.

“So why should I buy this company’s stock?”

An Equity Story is created to answer that question. Instead of listing numbers like revenue or profit, it explains in one flow what problem the company started from, what choices it made to build competitiveness, and why that structure can continue to work in the future. In other words, before talking about numbers, it shows why those numbers are inevitable.

Equity Story: structure matters more than results

Revenue and profit are past results, but investors want to know whether those numbers are one-off or sustainable. This includes elements that competitors cannot easily copy, such as technological barriers, cost structures, and market position. A strong Equity Story explains how past decisions led to current performance, and how that performance logically connects to future growth.

For this reason, an Equity Story is usually built in three stages. The past explains what problem the company identified and why it entered the industry. The present shows how those choices became competitive advantages and what position the company holds in the market. The future connects how that competitiveness leads to market expansion and profit growth. The more seamlessly these three stages are linked, the more persuasive the story becomes.

For example, for an electric vehicle company, saying “last year’s revenue was $686 million” does not complete an Equity Story. Instead, it should explain that the company focused early on battery efficiency as a key bottleneck, secured cost competitiveness as a result, can protect margins even as price competition intensifies, and can eventually expand into autonomous driving or energy storage markets. The numbers should follow as evidence that supports this story.

The real role of an Equity Story

When the market is strong, anyone can talk about growth. When stock prices fluctuate, the criterion investors use to decide whether to keep holding is the Equity Story. That is why it is not just IR material, but closer to a worldview that explains how the company creates value. Its core role is to make investors think, even after recognizing the risks, “this is still a company worth holding.” |

|

|

Send us any suggestions you’d like to share while reading Bitter’s newsletter! |

|

|

Advertising, inquiries : viter@thevistapartners.com / Published by Newstop. Unsubscribe |

|

|

|

|